Coffee – from plant to cup. What does it really cost?

By Xavier Crowley

Bean juice. Cuppa joe. The good stuff. The elixir of life. Coffee.

Throughout the UK in the good ol’ 1600s, the median breakfast drink of choice was beer. But then along comes coffee on its push to become the world’s favourite stimulant, with around two billion cups a day drank globally today, and it’s no coincidence the enlightenment started soon after. Turns out, starting your day with an energy-providing, memory-enhancing drug is better than being intoxicated.

Back home in Australia, people consume slightly less than a cup per person per day from instant, pods, espresso, filter, clever dripper, aeropress, or any number of types of coffee. Homing in on store prices, we pay on average ~$3.99 a latte or other milk-based drink, or a little less for non-milk drinks. Not the biggest dent in the wallet, but as we’ll soon explore, a combination of climate risks among other factors are threatening to push that price up.

Buckle up, as we’ll be going step by step through the costs of coffee, social and monetary, from the farmers across the world to the rents that stores pay. This is a long one, so feel free to jump to any section that interests you!

Australia is in pretty good economic shape, but will the end of JobKeeper change that?

By Maxwell Ward

Covid? What Covid? From what I’ve seen the pubs and clubs are bustling, sports stadiums are getting crowds, believers are congregating in their places of worship and woah this light rail to campus is actually kind of crammed.

With the first vaccines being rolled out in Australia last week, life is returning to back to the good old days right?

Well, yes and no. Economic forecasts are certainly looking positive with Deloitte Access Chief Economist Chris Richardson stating “we got this” in response to his outlook on business conditions for 2021.

From Doomsday Preppers to Pandemic, Netflix has released a variety of shows to get you ready for the looming ‘apocalypse’. Whilst humanity has a great challenge ahead of itself, I certainly don’t think Netflix is a suitable method of preparation for what is yet to come.

A more realistic problem appearing on the horizon is the threat of a second Great Depression, one that has the potential to have a more thorough and wider impact than its predecessor. Economic trends are beginning to mirror the hardships that workers of the 1930s had to face and if government’s fail to get stimulus packages through the halls of parliament and into the industries that need it most, a recession may become the least of our worries.

Interest rate cuts may have provided a temporary reprieve to the economy but at the cost of inflating long-term economic risks.

Remember the last time you waited in line at your favourite café, thinking about the RBA’s decision to change interest rates? What impact would it have on your decision to buy that extra croissant?

If you said yes you’re either lying or you really love Economics!

If you’ve been listening to the news for the past couple of months, you would’ve heard about the Royal Commission into Misconduct in the Banking, Superannuation and Financial Services Industry.

With the public image of Australia’s biggest and oldest banks taking a battering during this royal commission, you may have been wondering if you could switch banks—you may feel as though you have no other alternative but to use one of the Aussie “Big Four” banks, namely the Commonwealth Bank (CBA), ANZ, Westpac, and NAB.

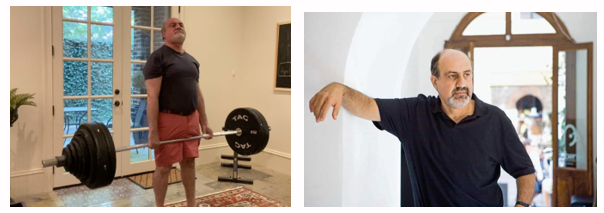

Allow me to introduce you to our eccentric and highly regarded subject; Nicholas Nassim Taleb (NNT). NNT is the author of books such as The Black Swan, Skin in the Game and Antifragile. He is a highly successful derivatives trader, hedge fund manager, statistician, and graduate of both the University of Paris (PhD in management science) and the University of Pennsylvania, Wharton (MBA). He grew up during the Lebanese civil war, is a self-described flaneur (an observant lounger) and is obsessed with deadlifts. The Most important biographical fact you need to know is that he despises what you are learning (assuming you are an Economics student).

Picture Related: Nassim Taleb pulling like a gorilla, fuelled by the tears of Economists

I recently finished his 5 book essay, the Incerto. Here are some thought provoking quotes I have gathered;

“ An economist is a mixture of 1) a businessman without common sense, 2) a physicist without brain , and 3) a speculator without balls”

“Those with brains no balls become mathematicians, those with balls no brains join the mafia, those with no balls no brains become economists.”

“To have a great day: 1) Smile at a stranger, 2) Surprise someone by saying something unexpectedly nice, 3) Give some genuine attention to an elderly, 4) Invite someone who doesn’t have many friends for coffee, 5) Humiliate an economist, publicly, or create deep anxiety inside a Harvard professor”

“Being nice to the wicked (or economist) is equivalent to being nasty with the virtuous.”

[On his greatest disappointment]:” That I am unable to destroy the economics establishment.”

So, why all the hate?

NNT’s position on modern economists stems from Paul Samuelson. For those unacquainted, this is the guy that introduced and integrated mathematics into modern economics. From his work, other academics were able to pioneer Econometrics. NNT being a statistician, has some pretty major qualms with Econometrics as a field, especially considering its prevalence in academic literature. Just about every Economics research paper relies on Econometrics for methodology. With these mathematical models comes the assumptions such as ceterus paribus (all else being equal), or ‘rationality’.

The study of Econometrics is further complicated when you consider exactly what Economists set out to do. They want to understand material welfare in order to increase it. To do so, they have to work in the aggregate, on the nation sized scale. According to NNT, this is simply an impossibility.

The reliance on econometrics has brewed a passionate dislike and distrust of most Economists for NNT. Economics is not axiomatic, that is to say it can’t rely on principles because its principles are derived from us, people. You can’t predict people down to a tee and it’s a fundamental issue Economists have grappled with from the 20th century onward. Given NNT’s palpable obsession with quantitative finance, this really rubbed him the wrong way.

Skin in the game: are Economists ‘charlatans’ ?

NNT’s namesake book Skin in the Game is essential in understanding his position on Economics and the social sciences more broadly. Academics are more than willing to provide their opinions and politicians and decision makers are more than willing to lap it up. Now, when politicians enact faulty policy who is to blame? The politician or the expert that convinced them it was a great idea? What’s more is that Economists can and do get it wrong.[1] So, you have an Economist carrying out work that cannot and will not be exact. Said work will influence policy, which materially influences society and your wellbeing and the truth is we cant exactly know how this policy will benefit you personally, your community and sometimes the country itself.

So, once again, who do we blame? Who gets sacked for a faulty policy? Most likely the politician because they need to be re-elected. The Economist, however, has no skin in the game with this. For proof, take Paul Kraugman’s (Nobel Laureate) prediction that:

“By 2005 or so, it will become clear that the Internet’s impact on the economy has been no greater than the fax machine’s.”

Or take Milton Friedman’s (Nobel Laureate) take that the only social responsibility a corporation has is to maximise shareholder wealth (the environment is #notmyproblem).

Or take the current Nobel Laureates[2]; They proved empirically that minimum wages do not result in the unemployment we thought it did, despite 300 years of literature saying it does.

Anecdotally, two Nobel Laureates and 300 years of economic research are wrong. They informed policy, Friedmann on his own re-invented the post-war western economy. Yet their mistakes never catch up with them despite the danger and implications they can have on you.

This is defined as moral hazard and occurs when an individual has the incentive to take on risk because they do not bear the full costs of that risk. If Milton Friedman had his future threatened by global warming on an existential level, I don’t think he’d have the same opinions. Yet, as an individual he would be more than willing to take on the risk that his ideas do not work because its not his problem. Even if being wrong affects the Economist tangibly, the effects of their screw up can never be reflected in their punishment because their effect on people is in policy and therefore prolific.

Black Swan theory: all it takes is one W or one L

NNT is a champion of black swan theory; some calamities in life are so incredibly unpredictable that we never even try to prevent them. As a derivatives trader, NNT saw entire careers boom and bust in hours because of individual bets. He saw firsthand the life changing effects of black swans and he found that the traders never thought they would be so successful or so unprofitable off of a single trade. He applies this to the possible effects of the Economist. Because of the privileged platform they often have, and the general good they do (Economists are generally good), society never insulates itself from a single misaligned theory or policy. A policy could even be successful for an extended period before the consequences start to show. Either way, we never stop and revise the dominant economic theory because it works, people are making money and are living good lives. That is exactly what the financial sector thought pre-GFC, it’s how policy makers felt before the OPEC oil crisis turned the lights off and it’s how we all felt before COVID decimated global supply chains and delayed our packages for weeks (terrible, I know).

Huh, guess that’s why they call it the dismal science….

[1] No Economist was worried enough about financial regulation to consistently float ideas to policy makers before the GFC, the only people who predicted it had skin in the game (hedge funds and traders). No social scientist or political expert thought the Soviet Union would collapse soon, and then all of a sudden it vanished over night